GST Goods and Service Tax

Presented by ®

Date: 19-March 2017

For internal use of Miracle Accounting Software.

Prepared By Chirag Ruparel(7621045045)

૧. જી.એસ.ટી. કોન્સે પ્ટ

જી.એસ.ટી. કોન્સેપ્ટ

જી.એસ.ટી. શ ું છે ? • ગડ્ઝ એન્ડ સર્વિસ ટેક્ષ. • • • •

જી.એસ.ટી.: સૌથી મોટો ટે ક્ષ રિફોમમ

૧૧ જેટલા ઇન્ડાયિે ક્ટ ટે ક્ષ મર્જ થશે

ડેસ્ટીનેશન બેઝ્ડ ટેક્ષ: ટેક્ષની અસિ સીધી ડેસ્ટીનેશન એટલે કે કન્સ્યમિ પિ ડયઅલ કુંટ્રોલ મેકેનીઝમ(સેન્ટ્રલ અને સ્ટે ટ)

3

જી.એસ.ટી. કોન્સેપ્ટ

જી.એસ.ટી. શા માટે ? હાલ ના ટેક્ષ સ્ટ્રક્ચિ માું અમક મયામદાઓ છે :

• • • • •

ડબલ ટેક્ષની પદ્ધર્િ

કાસ્કેડીંગ ઈફેક્ટ જરટલ વહીવટીકિણ િાજ્યો વચ્ચે ટેક્ષની એકરૂપિા નો અભાવ

ગડ્ઝ અને સર્વિસ વચ્ચે ના ર્વવાદ

આ બધી મયામદાઓને ર્નવાિવા GST અમલમાું મકાશે.

4

જી.એસ.ટી. કોન્સેપ્ટ

ડેસ્ટીનેશન બેઝ્ડ ટેક્ષ નો કોન્સેપ્ટ • • • •

કન્ઝપ્શન બેઝ્ડ ટેક્ષ

જ્યાું કન્ઝપ્શન થશે િે િાજ્ય ટે ક્ષ વસલ કિશે

ઓછા ડેવ્લોપ્ડ િાજ્યો માટે વિદાન એક્સપોટમ = કોઈ જ ટે ક્ષ નરહ.

5

જી.એસ.ટી. કોન્સેપ્ટ

હાલન ું ટેક્ષ સ્ટ્રક્ચિ

6

જી.એસ.ટી. કોન્સેપ્ટ

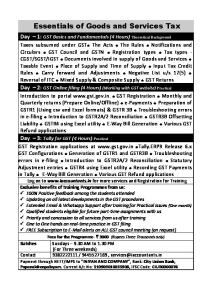

હાલ ના ક્યા ટેક્ષ GST માું ભેળવાઈ જશે ? કેન્દ્ર દ્વારા લેવામાાં આવતા કર

રાજ્ય દ્વારા લેવામાાં આવતા કર

a. Central Excise duty

a. State VAT

b. Duties of Excise

b. Central Sales Tax

•

Medicinal and Toilet Preparations

c. Additional Duties of Excise

c. Taxes on advertisements d. Taxes on lotteries, betting and gambling

•

Goods of Special Importance

e. Entertainment and Amusement Tax (except when levied by the local bodies)

•

Textiles and Textile Products

f. State Surcharges and Cesses (so far as they relate to supply of goods and services)

d. Additional Duties of Customs (CVD)

g. Entry Tax (all forms)

e. Special Additional Duty of Customs (SAD)

h. Luxury Tax

f. Service Tax

i. Purchase Tax

g. Central Surcharges and Cesses.

7

જી.એસ.ટી. કોન્સેપ્ટ

8

હાલ ના ક્યા ટેક્ષ GST માું ભેળવાઈ જશે ? Excise /Cess

Serv. Tax /Cess

CVD

SAD

CGST

VAT

Entry Tax

Octroi /LBT

Luxury /Ent. Tax

SGST

જી.એસ.ટી. કોન્સેપ્ટ

હાલ ના ક્યા ટેક્ષ GST પછી પણ િહેશે ? a. Basic Custom Duty b. Stamp Duty c. Property Tax d. Electricity Duty e. Road Tax

f. Toll Taxes g. Export Duty h. Professional Tax i. Tax on Alcohol

9

૨. ડયઅલ જી.એસ.ટી.

ડયઅલ જી.એસ.ટી.

ડયઅલ જી.એસ.ટી. કેવી િીિે કામ કિશે?

• CGST અને SGST એમ બન્ને ટેક્ષ એક સાથે લાગશે • CGST = સેન્ટ્રલ જી.એસ.ટી. (કેન્ર રાિા વસલ કિવામાું આવશે) • SGST = સ્ટેટ જી.એસ.ટી. (િાજ્ય રાિા વસલ કિવામાું આવશે)

11

ડયઅલ જી.એસ.ટી.

ડયઅલ જી.એસ.ટી. ન ું સ્ટ્રક્ચિ SUPPLY

TAX

Intra State Supply

CGST SGST

Inter State Supply

IGST

Import

BCD IGST (in place of CVD and SAD)

Exports

Zero rated

12

ડયઅલ જી.એસ.ટી.

સ્ટેટ જી.એસ.ટી. (SGST) • નીચેના જે કિ છે

• વેટ, મનોિું જન કિ, લકઝિી કિ • લોટિી-બેરટિંગ-જગાિ પિનો કિ • િાજ્યોના સેઝ અને સિચાર્જ • એન્ટ્રી ટેક્ષ, ઓકટ્રોય, એલ.બી.ટી. વગેિે...

આ બધા કિ ના બદલામાું િાજ્ય સિકાિ દ્વાિા SGST લેવામાું આવશે.

13

ડયઅલ જી.એસ.ટી.

સેન્ટ્રલ જી.એસ.ટી. (CGST) • નીચેના જે કિ છે

• એક્સાઈઝ ડયટી

• વધાિાની એક્સાઈઝ ડયટી • સર્વિસ ટેક્ષ • વધાિાની કસ્ટમ ડયટી વગેિે...

આ બધા કિ ના બદલામાું કેન્ર સિકાિ દ્વાિા CGST લેવામાું આવશે.

14

ડયઅલ જી.એસ.ટી.

ઇન્ટીગ્રેટેડ જી.એસ.ટી. (IGST) • • • •

IGST એ ડેસ્ટીનેશન બેઝડ ટેક્ષ ન ું મહત્વન પરિબળ ગણી શકાય IGST એ કેન્ર સિકાિ ને મળવા પાત્ર વેિો છે દિે ક પ્રકાિના આંિિ િાજ્ય વ્યવહાિો માું IGST લાગ પડશે

આ વ્યવહાિોમાું આંિિ િાજ્ય સ્ટોક ટ્રાન્સફિનો પણ સમાવેશ થાય છે

• IGST = CGST + SGST

15

ડયઅલ જી.એસ.ટી.

16

ઇન્ટ્રા સ્ટે ટ સપ્લાઈ ન ું હાલ ન ું સ્ટ્રક્ચિ મેન્યફેક્ચિિ

એક્સાઈઝ ડયટુ ી

વેટ

ટ્રે ડિ

એક્સાઈઝ ડયટુ ીની કોસ્ટ

વેટ

સર્વિસ પ્રોવાઇડિ

સર્વિસ ટેક્ષ

ડયઅલ જી.એસ.ટી.

17

ઇન્ટ્રા સ્ટેટ સપ્લાઈન જી.એસ.ટી. પછીન સ્ટ્રક્ચિ મેન્યફેક્ચિિ

સી. જી.એસ.ટી.

એસ. જી.એસ.ટી.

ટ્રેડિ

સી. જી.એસ.ટી.

એસ. જી.એસ.ટી.

સર્વિસ પ્રોવાઇડિ

સી. જી.એસ.ટી.

એસ. જી.એસ.ટી.

ડયઅલ જી.એસ.ટી.

18

ઇન્ટિ સ્ટે ટ સપ્લાઈન હાલ ન ું સ્ટ્રક્ચિ મેન્યફેક્ચિિ

એક્સાઈઝ ડયટુ ી

સી.એસ.ટી.

ટ્રે ડિ

એક્સાઈઝ ડયટુ ી ની કોસ્ટ

સી.એસ.ટી.

સર્વિસ પ્રોવાઇડિ

સર્વિસ ટેક્ષ સી.એસ.ટી.= સેન્દ્રલ સેલ્સ ટે ક્ષ

ડયઅલ જી.એસ.ટી.

19

ઇન્ટિ સ્ટેટ સપ્લાઈન જી.એસ.ટી પછીન સ્ટ્રક્ચિ મેન્યફેક્ચિિ

આઈ. જી.એસ.ટી.

ટ્રે ડિ

આઈ. જી.એસ.ટી.

સર્વિસ પ્રોવાઇડિ

આઈ. જી.એસ.ટી. આઈ.જી.એસ.ટી.= સી.જી.એસ.ટી. + એસ.જી.એસ.ટી.

ડયઅલ જી.એસ.ટી.

20

ગડ્ઝ અથવા સર્વિસની ઈમ્પોટે ડ સપ્લાઈન હાલન સ્ટ્રક્ચિ મેન્યફેક્ચિિ

કસ્ટમ્સ ડયટુ ી

CVD + SAD

ટ્રેડિ

કસ્ટમ્સ ડયટુ ી

CVD + SAD

સર્વિસ પ્રોવાઇડિ

સર્વિસ ટેક્ષ

CVD=Countervailing Duties SAD= Special Additional Duty of Customs

ડયઅલ જી.એસ.ટી.

21

ગડ્ઝ અથવા સર્વિસની ઈમ્પોટે ડ સપ્લાઈન જી.એસ.ટી. પછીન સ્ટ્રક્ચિ મેન્યફેક્ચિિ

કસ્ટમ્સ ડયટુ ી

આઈ. જી.એસ.ટી.

ટ્રે ડિ

કસ્ટમ્સ ડયટુ ી

આઈ. જી.એસ.ટી.

સર્વિસ પ્રોવાઇડિ

આઈ. જી.એસ.ટી.

ડયઅલ જી.એસ.ટી.

22

વેિા ના દિ • • • • •

શન્ય દિ (નીલ િે ઈટેડ)

0

સોના ચાુંદી જેવી કીમિી વસ્તઓ પિ (લોઅિ િે ઈટ)

૫%

જીવન જરૂિીયાિ ની વસ્તઓ ઉપિ નીચો દિ (મેિીટ િે ઈટ)

૧૨ %

સામાન્ય ચીજ વસ્તઓ ઉપિ સમાન દિ (સ્ટાન્ડડમ િે ઈટ)

૧૮ %

લકઝિી માલ ઉપિ ઉંચો દિ (ડી-મેિીટ િે ઈટ)

૨૮ %

ડયઅલ જી.એસ.ટી.

23

જી.એસ.ટી. ની અસિ ઉદાહિણ દ્વાિા સમજીએ

Cont.….

ડયઅલ જી.એસ.ટી.

24

જી.એસ.ટી. ની અસિ ઉદાહિણ દ્વાિા સમજીએ Cont.….

167706

–

165044

= 2662/-

ડયઅલ જી.એસ.ટી.

થ્રેશોલ્ડ લીમીટ • વાર્ષિક ટનોવિ < ૨૦ લાખ • વાર્ષિક ટનોવિ < ૧૦ લાખ (નોથમ ઇસ્ટનમ અને રહલ સ્ટેટ્સ) • વાર્ષિક ટનોવિ < ૧.૫ કિોડ • વાર્ષિક ટનોવિ > ૧.૫ કિોડ

િાજ્યન ું અર્ધકાિક્ષેત્ર િાજ્ય અથવા કેન્ર ન ું અર્ધકાિક્ષેત્ર

નોંધ: અર્ધકાિક્ષેત્ર ર્વશેની લીમીટ ર્વષે હજ ચચામઓ ચાલી િહી છે માટે હાલ પિત ું િેને અંદાજીિ આકડા િિીકે ગણી શકાય.

25

ડયઅલ જી.એસ.ટી.

ઉચક વેિાની જોગવાઈ(કમ્પોઝીસન સ્કીમ ) • વાર્ષિક ટનોવિ < ૫૦ લાખ થત ું હોય ત્યાું સધી ઉચક વેિાનો ર્વકલ્પ મળી શકે • ઉચક વેિા અંિગમિ આશિે ૨% કિ હોવાની સુંભાવના છે

• જો કોઈ વ્યક્ક્િ ઇન્ટિ સ્ટેટ સપ્લાઈ કિત હોય િો િે ઉચક વેિાનો ર્વકલ્પ સ્વીકાિી શકશે નરહ.

• ઉચક વેિાનો ર્વકલ્પ સ્વીકાિનાિ વ્યક્ક્િ વેિો ઉઘિાવી શકશે નરહ. • આ ઉપિાુંિ ITC પણ બાદ મળશે નરહ.

26

૩. સપ્લાઈ નો કોન્સેપ્ટ

સપ્લાઈ નો કોન્સેપ્ટ

સપ્લાઈ કોને કહેશ?ું • સપ્લાઈ ની અંદર

• વેચાણ, ટ્રાન્સફિ, બાટમ િ, એક્સચેન્જ, લાયસન્સ, લીઝ, ભાડે આપવ ું વગેિે નો સમાવેશ થાય છે .

• કોઈ પણ િીિે માલ કે સેવાઓ નો અવેજ ના બદલા માું ધુંધા દિર્મયાન કે ધુંધા ના ર્વકાસ માટે ર્નકાલ કિવો.

• સપ્લાઈ માટે બે પક્ષકાિન ું હોવ ું કે માલલકી ટ્રાન્સફિ થવી જરૂિી નથી. • એક જ કુંપનીની એક બ્રાન્ચ માથી બીજી બ્રાન્ચમાું માલ કે સેવા ટ્રાન્સફિ થવી એ પણ સપ્લાઈ ગણાશે. • ઈ-કોમસમ દ્વાિા પ ૂિી પાડવામાું આવેલ બ્રાન્ડેડ સર્વિસીસ • આ બધીજ સપ્લાઈ પિ વેિો લાગશે.

28

29

સપ્લાઈ નો કોન્સેપ્ટ

માલ સપ્લાઈ થયેલ ક્યાિે ગણાશે ? • નીચેમાથી જેની િાિીખ પહેલા હશે િે િાિીખે માલ સપ્લાઈ થયેલ ગણાશે 1. માલ ખસેડી શકાય િેમ હોય ત્યાિે જે રદવસે માલ પ્રાપ્િ કિનાિ ને માલ ખસેડવામાું આવે િે રદવસ

2. માલ ખસેડી શકાય િેમ ન હોય ત્યાિે માલ હવાલે કિવામાું આવે િે રદવસ સપ્લાઈ ના બીલની િાિીખ સપ્લાઈન ું પેમેન્ટ પ્રાપ્િ કાયમની િાિીખ માલ મેળવનાિના ચોપડે માલ મળ્યાની નોંધ કિવામાું આવે િે િાિીખ Cont...

સપ્લાઈ નો કોન્સેપ્ટ

માલ સપ્લાઈ થયેલ ક્યાિે ગણાશે ? Cont...

3. જયાિે માલ જુંગડ/ચલણથી મોકલેલ હોય િેમા જયાિે સપ્લાય થવાન નક્કી થાય અથવા માલ મોકલ્યા થી છ માસ નો સમય

બે માથી જે વહેલ ું હોય િે રદવસ સપ્લાઈ થયેલ ગણાશે

4. િીટન્સમ ભિવામાું આવે િે િાિીખ 5. CGST અને SGST ન ું ચકવણ ું કિવામાું આવે િે િાિીખ

30

સપ્લાઈ નો કોન્સેપ્ટ

સપ્લાઈ ઓફ સર્વિસ ક્યાિે થઇ ગણાય? 1. સમયસિ બીલ અપાિી સર્વિસીસ બીલની િાિીખ ચકવણ ું મળ્યા ની િાિીખ ચોપડે નોધ કયામની િાિીખ

2. સિિ(Continuous) સપ્લાઈ ગણાિી સેવાઓ ચકવણ ું કિવાની િાિીખ બીલ ની િાિીખ ચકવણ ું મળ્યાની િાિીખ સેવા પ ૂિી થાય િે િાિીખ

3. િીવસમ ચાર્જ બેસીસ પિ સેવા મેળવનાિ સેવા મળ્યાની િાિીખ

બીલ મળ્યાની િાિીખ પેમેન્ટ કયામની િાિીખ ચોપડે નોધ કયામની િાિીખ

4. કિાિ હેઠળ ની સેવાઓ સેવા પ ૂિી થાય િે િાિીખ

5. ઉપિ માથી કોઈ િીિે નક્કી ના થઇ શકે િો િીટન્સમ ભિવાની િાિીખ CGST કે SGST ન ું ચકવણ ું કિવામાું આવે િે િાિીખ

31

૪. ઈનપટ ટે ક્ષ ક્રેડીટ

ઈનપટ ટેક્ષ ક્રેડીટ Used or intended to be used

Return has been furnished

Tax charged for supply has been paid

Has received the goods and/or services

33

Input Credit

In the course or furtherance of Business

Possession of tax invoice, D/N, etc.

ઈનપટ ટેક્ષ ક્રેડીટ

ઈનપટ ટેક્ષ ક્રેડીટ મેળવવાની શિિો • વેપાિી પાસે માલ/સેવાઓ ઉપિ ચ ૂકવેલ વેિાની ક્રેડીટનો દાવો કિવા પ્રથમ િેન ું મ ૂળ બીલ હોવ ું જરૂિી છે . • વેપાિીને િે માલ/સેવાઓ મળે લી હોવી જોઈએ, એટલે કે ફીઝીકલ માલ/સેવા મળે લ હોવી જોઇયે • વહેચનાિે િે ટેક્ષ ટ્રેઝિીમાું ચ ૂકવેલ હોવો જોઇયે(િોકડે થી/ ITC થી)

• ટેક્ષ ક્રેડીટનો દાવો કિનાિ વેપાિીએ િીટન્સમ ભિે લા હોવા જોઈએ, એટલે કે ટેક્ષ ક્રેડીટ બાદ લેનાિે પોિે િીટન્સમ ભિે લા હોવા જોઇએ.

• કોન્ટ્રાક્ટ ટાઈપના ધુંધામાું કટકે કટકે આવેલ પેમેન્ટ મા કટકે કટકે બનવેલ બીલ અને પેમેન્ટ હોવા છિાું કોન્ટ્રાક્ટન ફાઈનલ પેમેન્ટ ન બીલ બને િે મજબ ટેક્ષ ભિે લ હશે િો જ સમગ્ર કોન્ટ્રાક્ટની પેમેન્ટની િકમની ઈનપટ ટેક્ષ ક્રેડીટ નો દાવો થઇ શકશે.

34

ઈનપટ ટેક્ષ ક્રેડીટ

35

ઈનપટ ટેક્ષ ક્રેડીટ શાની મળશે ? માલ/સેવાઓ પ્રાપ્િ કિિી વખિે ચ ૂકવેલ વેિાની ઈનપટ ટેક્ષ ક્રેડીટ ર્નયમોથી ર્નદે શ કિે લ શિિો

અને ર્નયુંત્રનો ના આધાિે મળવાપાત્ર િહેશે:

• ફિજીયાિ િજીસ્ટ્રેશન નુંબિ મેળવાનો થિો હોય િેના ૩૦ રદવસ માું િજીસ્ટ્રેશન નુંબિ મેળવવા અિજી કિે લ હોય.

• મિજજયાિ િજીસ્ટ્રેશન નુંબિ મેળવેલ હોય િેઓને. • ઉચ્ચક વેિો ભિનાિ કિપાત્ર વ્યક્ક્િ સામન્ય જોગવાઈ મજબ વેિો ભિવા જવાબદાિ થાય.

• માલ કે સેવાઓ આંર્શક િીિે વેપાિ ના કાિણોસિ અને અંશિઃ િીિે અન્ય કાિણોસિ ઉપયોગ માું લેવામા આવે િો જેટલે અંશે વેપાિ માટે ઉપયોગ મા લેવાયેલ હોય િેટલે અંશે ઈનપટ ટે ક્ષ ક્રેડીટ મળવાપાત્ર.

ઈનપટ ટેક્ષ ક્રેડીટ

ઈનપટ ટેક્ષ ક્રેડીટ શાની નરહ મળે ? નીચેના સુંજોગોમાું માલ કે સેવાઓ પ્રાપ્િ કિિી વખિે વેિો ચ ૂકવેલ હોય િો પણ ઈનપટ ટેક્ષ ક્રેડીટ મળવા પાત્ર િહેશે નરહ:

• મોટિ વ્હીકલ નો ખાનગી અને વ્યક્ક્િગિ ઉપયોગ થયેલ હોય • કમમચાિીના પોિાના ઉપયોગ માટે આપવામાું આવિી સગવડિાઓ • કેટરિિંગ, ખાણી-પીણી, કલબની મેમ્બિર્શપ, વીમો, ટ્રાવેલ બેર્નરફટ, બ્યટી ટ્રીટમેન્ટ, પ્લાસ્ટીક સર્જિી, વગેિે..

• ઉચ્ચક વેિાનો લાભ લીધેલ વેપાિી પાસેથી કિવામા આવેલ ખિીદી

36

ઈનપટ ટેક્ષ ક્રેડીટ

37

ઈનપટ ટે ક્ષ ક્રેડીટ સિભિ શાની સામે થશે? ITC

CGST

CGST

IGST

SGST

IGST

SGST

IGST

IGST

CGST

SGST

ઈનપટ ટેક્ષ ક્રેડીટ

ઈનપટ ટેક્ષ ક્રેડીટ ઉદાહિણ

38

ઈનપટ ટેક્ષ ક્રેડીટ

ઈનપટ ટેક્ષ ક્રેડીટ ઉદાહિણ

39

જી. એસ. ટી. સેમ્પલ બીલ ફોિમેટ

* This is an indicative format based on invoicing rules

40

જી. એસ. ટી. સેમ્પલ લાઇબ્બ્લરટ લેજિ

* This is an indicative format based on invoicing rules

41

જી. એસ. ટી. સેમ્પલ કેશ લેજિ

* This is an indicative format based on invoicing rules

42

જી. એસ. ટી. સેમ્પલ ક્રેડીટ લેજિ

* This is an indicative format based on invoicing rules

43

૫. િજીસ્ટ્રે શન

િજીસ્ટ્રેશન

િજીસ્ટ્રેશન નુંબિન ું સ્ટ્રક્ચિ

State 1

• • • • • •

45

PAN

2

3

4

5

6

7

8

9

10

11

Entity

Blank

Check

13

14

15

12

િજીસ્ટ્રેશન નુંબિ ૧૫ ડીજીટનો હશે પ્રથમ ૨ ડીજીટ જે િે િાજ્યને ર્નરદિ ષ્ટ કિશે.

(ગજિાિ માટે ’૨૪’ ડીજીટ છે )

૩ થી ૧૨ નુંબિના ડીજીટ PAN નુંબિના હશે.

૧૩મો ડીજીટ િાજ્યમાું િેના કેટલા નુંબિ છે િે દશામવશે. ૧૪મો ડીજીટ હાલમા એક્સ્ટ્રા ડીજીટ િિીકે ખાલી િાખેલ છે જે અત્યાિે Z હશે. ૧૫મો ડીજીટ એ ચેકસમ હશે. (Checksum)

• ઉદાહરણ :

State 2

4

PAN A

A D F R 7

1

5

6

H

Entity

Blank

Check

1

Z

5

િજીસ્ટ્રેશન

46

િજીસ્ટ્રેશન માટે નક્કી કિે લ લીમીટ Aggregate Turnover

Region

Liability to Register

Liability for Payment of Tax

North East India

Rs 9 Lakhs

Rs 10 Lakhs

Rest of India

Rs 19 Lakhs

Rs 20 Lakhs

૬. િીટન્સમ

િીટન્સમ

િીટન્સમ કોણે ભિવા પડશે • એ દિે ક નોંધાયેલ કિપાત્ર વ્યક્ક્િ કે જે ટેક્ષ પેમેન્ટ માટેની Threshold લીમીટ ક્રોસ કિિા હોય

• આ ઉપિાુંિ

• ઇન્ટિ સ્ટેટ સપ્લાયસમ • TDS ડીડકટસમ અને ડીડકટી • ઈ-કોમસમ ઓપિે ટસમ • સપ્લાયસમ કે જે ઈ-કોમસમ ઓપિે ટસમ દ્વાિા સપ્લાઈ કિિા હોય

48

િીટન્સમ

રીટનનમાાં ક્ાાં પ્રકારની આઉટવડન સપ્લાઈની ર્વગતો રરવાની રહેે ે ? • • • • • •

િજીસ્ટડમ વ્યક્ક્િને કિે લ આઉટવડમ સપ્લાઈ

અન-િજીસ્ટડમ વ્યક્ક્િને કિે લ આઉટવડમ સપ્લાઈ(કન્સ્યમિ) ક્રેડીટ અને ડેબીટ નોટ્સ ની ર્વગિો

નીલ િે ટેડ, એકઝમ્પ્ટડ અને નોન જી.એસ.ટી. સપ્લાઈ એક્સપોટમ સ

ભર્વષ્યમા કિવાની સપ્લાઈ માટે મળે લ એડવાન્સ વગેિે...

49

િીટન્સમ

50

ે ે કે કેમ? દિે ક બીલ ની ઇન્ફોમેશન અપલોડ કિવાની િે હશ • B2B = લબઝનસ ટ લબઝનસ • આમાું દિે ક સપ્લાઈ (ઇન્ટિ સ્ટેટ/ઇન્ટ્રા સ્ટેટ) માટે ઇન્વોઇસ અપલોડ કિવાની િે હશ ે ે • કારણ: સપ્લાઈ મેળવનાિ વ્યક્ક્િને ITC મેળવવા માટે ઇન્વોઇસ મેચ થવી જરૂિી છે . • B2C = લબઝનસ ટ કન્સ્યમિ • જનિલી આના માટે ઇન્વોઇસ અપલોડ કિવી જરૂિી નથી

• કારણ: સપ્લાઈ મેળવનાિ વ્યક્ક્િ ITC ની જરૂિ નથી. •

પણ જો ઇન્ટિ સ્ટે ટ સપ્લાઈ હોય ત્યાિે જો ૨.૫ લાખ થી વધ ઇન્વોઇસ વેલ્ય હોય િેવા કેસ માું ઇન્વોઇસ અપલોડ કિવાની િહેશે

• એ ર્સવાયની દિે ક ઇન્ટિસ્ટેટ/ ઇન્ટ્રાસ્ટેટ સપ્લાઈ માટે અગ્રીગેટ સ્ટેટ વાઈઝ સમિી આપવાની િહેશે

િીટન્સમ

51

Regular Dealer Form Type Frequency Form GSTR-1 Form GSTR-2A Form GSTR-2 Form GSTR-1A

Due Date

Slide 1

Details to be Furnished

Monthly

10th of succeeding આઉટવડમ સપ્લાઈ month

Monthly

સપ્લાઈ મેળવનાિ વ્યક્ક્િ માટે , On 11th of સપ્લાયર દ્વારા બનાવાયેલ Form GSTR-1 પિથી ઓટો succeeding Month પોપ્યલ ું ેટેડ ઈન્વડમ સપ્લાઈ ની ર્વગિો

Monthly

15th of succeeding ઈનવડમ સપ્લાઈ (જેની ઈનપટ ટે ક્ષ ક્રેડીટ મળવા પત્ર હોય) Form GSTR-2A માું કઈ સધાિો હોય િો િે આમાું કિવાનો િહેશે month

Monthly

સપ્લાઈ મેળવનાિ વ્યક્ક્િએ Form GSTR-2 માાં ઉમેિેલી, 20th of succeeding સધાિે લી, અને ડીલીટ કિે લી આઉટવડમ સપ્લાઈ ની ર્વગિો month સપ્લાયિને આપવામાું આવશે

િીટન્સમ

52

Regular Dealer - Slide 2 Form Type Frequency Form GSTR-3 Form GSTR-9

Monthly

Due Date

Details to be Furnished

20th of succeeding આઉટવડમ સપ્લાઈ અને ઈનવડમ સપ્લાઈ ના બેઝીસ પિ મુંથલી month િીટન્સમ + ટે ક્ષ ની િકમના પેમેન્ટની સાથે વાર્ષિક િીટનમ – મળે લ ITC અને ચ ૂકવેલ GST ની ર્વગિો

Annually

31st Dec of next પિથી (જેમાું લોકલ, ઇન્ટિ સ્ટે ટ અને એક્સપોટમ /ઈમ્પોટમ નો fiscal સમાવેશ થાય છે )

િીટન્સમ

53

Aggregate Turnover Exceeds 1 crore Form Type Frequency Form GSTR-9B

Annually

Due Date

Details to be Furnished

Annual, 31st Dec of next fiscal

Reconciliation Statement – ઓડીટ કિે લ વાર્ષિક ખાિા અને

એક િીકન્સીલેશન સ્ટે ટમેન્ટ

િીટન્સમ

54

Composite Tax Payer Form Type Frequency Form GSTR-4

Quarterly

Due Date

Details to be Furnished

18th of succeeding આઉટવડમ સપ્લાઈ month (Includes auto populated details from GSTR-1)

િીટન્સમ

55

Foreign Non-Resident Taxpayer Form Type Frequency Form GSTR-5

Monthly

Due Date

Details to be Furnished

20th of succeeding ઈમ્પોટમ સ,આઉટવડમ સપ્લાઈ, મળે લ ITC, ચ ૂકવેલ વેિો, month / 7 Days after the expiry અને કલોલઝિંગ સ્ટોક ની મારહિી આપવી of Registration

િીટન્સમ

56

Input Service Distributor Form Type Frequency Form GSTR-6

Monthly

Due Date 13th of succeeding month

Details to be Furnished આપેલ ઈનપટ ક્રેડીટ ની મારહિી આપવી

(Includes auto populated details from GSTR-1)

િીટન્સમ

57

Tax Deductor Form Type Frequency Form GSTR-7 Form GSTR-7A

Due Date

Monthly

10th of succeeding month

Monthly

TDS certificate to be made available for download

Details to be Furnished કપાયેલ TDS ની મારહિી આપવી TDS સટીફીકેટ – જે વેલ્ય પિ TDS કપાયેલ હોય િેની મારહિી આપવી િેમજ કપાયેલ TDS ને સિકાિી ખાિા માું જમા કિવાની મારહિી આપવી

િીટન્સમ

58

E-commerce Form Type Frequency Form GSTR-8

Monthly

Due Date

Details to be Furnished

10th of succeeding month

ઈ-કોમસમ ઓપિે ટિ દ્વાિા કિાયેલ સપ્લાઈની મારહિી અને

િેના પિ વસલ કિાયેલ TAX ની મારહિી આપવી

િીટન્સમ

59

Final return • એવા કરપાત્ર વ્યક્ક્ત માટે કે જેન ાંુ રજીસ્રેે ન સરન્દ્ડર/કેન્દ્સલ કરે લ ાંુ છે . Form Type Frequency Form GSTR-10

Monthly

Due Date

Details to be Furnished

Within 3 months of cancellation of registration

ઇનપટ્સ અને કેર્પટલ ગડ્ઝ, ચ ૂકવેલ અને ચકવવા પત્ર ટે ક્ષ ની મારહિી આપવી.

િીટન્સમ

60

GSTR - 1 Outward Supply (Monthly by 10th)

GSTR - 2 Inward Supply (Monthly by 15th)

GSTR - 3 Regular Return (Monthly by 20th)

GSTR - 4 Compounding Scheme (Qrtly by 18th)

GSTR - 5 Non Resident Tax Payer (Monthly by 20th)

GSTR - 6 ISD (Monthly by 13th)

GSTR - 7 TDS Return (Monthly by 10th)

GSTR - 8 E-Commerce (Monthly by 10th)

GSTR - 9 Annual Return (By 31st Dec)

GSTR - 10 Surrendered/ Cancelled Within 3 months

૭. િીફન્ડ

િીફન્ડ

િીફન્ડ કોને કેહશ?ું • ભાિિ બહાિ ર્નકાસ કિે લ માલ/સેવાઓ અથવા કોઈ પણ સપ્લાઈ પિ લાગેલ ટે ક્ષ ન ું િીફન્ડ

• ભાિિ બહાિ ર્નકાસ કિવામાું આવેલ માલ/સેવાઓ માું વપિાયેલ ઈનપટ અથવા ઈનપટ સર્વિસીઝ

• વણ વપિાયેલ ઈનપટ ટે ક્ષ ક્રેડીટ ન ું િીફન્ડ (માત્ર નીચેના કેસ માાં મળવા પાત્ર) એક્સપોટમ ડયટી ન લાગિી હોય િેવા માલના ર્નકાસ પિ સર્વિસીસની ર્નકાસ પિ આઉટ્પટ ટેક્ષના દિ કિિા ઈનપટ ટેક્ષનો દિ વધાિે હોય િેવા કેસ માું

62

૮. GST કાઉન્સીલ અને GSTN

GST કાઉન્સીલ અને GSTN

GST કાઉન્સીલ • GST Council એ કેન્ર અને િાજ્ય સિકાિન ું સુંયક્િ મુંડળ છે , જેમાું કેન્રીય નાણા પ્રધાન – ચેિમેન િાજ્ય પ્રધાન – મહેસલ (Revenue) અને દિે ક િાજ્ય માથી સભ્ય િિીકે નાણા પ્રધાન અને કિવેિા પ્રધાન નો સમાવેશ થશે

• GST કાઉન્સીલ ન ું કાયમ GST અંગેના િમામ મહત્વ પ ૂણમ ર્નણમયો લેવા GST ના કિ, કેન્ર/િાજ્ય દ્વાિા લાગ પડિા સેસ અને સિચાર્જ વગેિે નક્કી કિવા ક્યા માલ અને સેવાઓ પિ GST લાગ પડશે અને શેના પિ એકઝમ્પશન િહેશે ટાનોવાિની Threshold લીમીટ નક્કી કિવી વગેિે..

64

GST કાઉન્સીલ અને GSTN

GSTN • GSTN એટલે ગડ્ઝ એન્ડ સર્વિસ ટેક્ષ નેટવકમ • જેન ું સર્જન GST ની જરૂિીયાિો ને સુંિોષવા થયેલ ું છે એમ કહી શકાય • કેન્ર/િાજ્ય સિકાિ/કિદાિાઓ/િોકાણકાિોને ને IT ઈન્રાસ્ટ્રક્ચિ અને સેવાઓ પ ૂિી પાડશે. • અન્ય મહત્વ ના કયો િજીસ્ટ્રેશન ની સેવાઓ સેન્ટ્રલ અને સ્ટેટ ઓથોિીટીઝ ને િીટનમસ ફોિવડમ કિવા IGST ની ગણિિી અને સેટલમેન્ટ

સેન્ટ્રલ અને સ્ટેટ ગવમેન્ટ ને અલગ અલગ પ્રકાિના MIS િે પોટટમ સ પિા પાડવા વગેિે...

• GSTN ના કાિણે કિ ભિવામાું સિળિા અને પાિદશમકિા િે હશ ે ે.

65

૯. GSP, ASP અને TRP

GSP, ASP અને TRP

GSP, ASP અને TRP શ ું છે ? • GSP – જી. એસ. ટી. સર્વધા પ્રોવાઇડિ • ASP – એપ્લીકેશન સર્વિસ પ્રોવાઇડિ • TRP – ટેક્ષ િીટનમ ર્પ્રપેિિ

67

GSP, ASP અને TRP

68

GSP, ASP અને TRP

69

ASP

GSP

TAX RETURN PREPARER

®

For internal use of Miracle Accounting Software.

Prepared By Chirag Ruparel(7621045045)