Finance and Synchronization A. Cesa-Bianchi1 1 Bank 2 Paris

J. Imbs2

J. Saleheen3

of England & Centre for Macroeconomics School of Economics (CNRS), and CEPR 3 Bank of England

July 2016

1

Disclaimer

The views expressed in this paper are solely those of the authors and should not be taken to represent those of the Bank of England.

Introduction

2

This paper I

We revisit a classic question in international macro: what is the impact of financial integration on business cycle synchronization?

I

International synchronization of cycles first-order question • Propagation of shocks, external constraint on macro policy,

coordination,... I

Old literature: openness in general main culprit • Historically, trade openness [Frankel and Rose (1998); Baxter and Kouparitsas (2005)]

I

Recent events shifted the focus on financial openness. Heuristically, it seems financial linkages helped propagate the great recession

Introduction

3

But theory is ambiguous I

Negatively correlated cycles in the International Real Business Cycle (IRBC) model [Backus et al (1992, JPE)]

• Idiosyncratic productivity shock leads to cross-country MPK differential • Because of efficient finance, resources shift where MPK is higher I

Positively correlated cycles in IRBC models with credit frictions and integrated financial markets [Allen and Gale (2000), Devereux and Yetman (2010), Dedola and Lombardo (2010)]

• Idiosyncratic shock (not necessarily to productivity) affects tightness of

the constraint at home • Because of financial integration, credit constraints are interdependent

across countries I

Key ingredient is idiosyncratic shock (ie, country-specific)

Introduction

4

Common shocks can have heterogeneous effects

I

Consider workhorse IRBC model with country heterogeneity (e.g. capital share) • Then purely common shock drives productivity up by same amount in

both countries (obviously) • But MPK increases more in country with low capital share I

As a result capital flows to high MPK country, outputs diverge, and synchronization falls

I

Observational equivalence between BKK with idiosyncratic shock vs. heterogeneous BKK with common shocks

Introduction

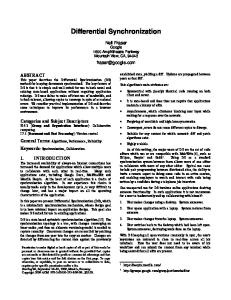

5

Impulse response functions in variants of BKK (A) Idiosyncratic shock to Home productivity (identical economies)

1

1.4

(B) Common shock to Home and Foreign productivity (heterogeneous economies) Home Foreign

1.2 0.8 1 0.8

0.6

0.6 0.4

0.4

0.2 0.2

0 -0.2

0 5

10

15

20

5

10

15

20

Note. Panel (A) reports the impulse response functions to a producivity shock in the Home country, in the case where the Home and Foreign economies are identical. The chart reports the response of Output in the Home (solid line) and Foreign (dashed line) economies. Panel (B) reports the same impulse response functions for a common shock (i.e., a shock that raises productivity by the same amount in the Home and Foreign economy) when the two economies are heterogeneous. The source of heterogeneity is the share of capital in the production function (θ). While in Panel (A), as in BKK, we set θ H = θ F = 0.36, in Panel (B) we set θ H = 0.44 and θ F = 0.32. All remaining parameters are identical to BKK (except for the time to build, set to 1). The size of the shock has been normalized so that it increases Home output by 1 percent.

Introduction

6

What is the effect of finance on synchronization

I

If objective is to test ambiguousc theory, then the focus should be on idiosyncratic, country-specific shocks.

I

Entails filtering out common shocks that are allowed to have different effects across countries.

I

Not done with the conventional trends / year effects, with consequences on these estimations.

Introduction

7

Common shocks

I

Common shocks constitute a key driver of business cycles • Large role of world and regional factor in developed countries (60% for

US, 72% for Canada, 72% for France, 56% for Germany) [Kose et al (2003, 2008), Crucini et al (2011)]

I

Empirically important to identify separately common shocks with country-specific loadings

I

We will show this is especially important in the literature on cycle synchronization

Introduction

8

Plan

I

Measures of business cycle synchronization & Common shocks

I

Estimation & Data

I

Results

I

Interpretation

I

Conclude

Introduction

9

Determinants of business cycle synchronization I

Frankel and Rose (1998, EJ), Imbs (2006, JIE): ρij = α + βKij + δTij + η ij,t where Kij is a measure of bilateral financial linkages, ρij Pearson correlation coefficient

I

Results: β > 0, δ > 0 ⇒ Positively correlated cycles

I

But if the true model is ρij,t = αij + βKij,t + δTij,t + η ij,t then the between result is fallacious. Need time series to check. Pearson correlation not adapted [Forbes-Rigobon (2002)]

Measures of business cycle synchronization & Common shocks

10

Determinants of business cycle synchronization (2) I

Period-by-period synchronization measure

[Giannone et al (2008), Morgan et

al (2004)]

Sij,t = − |yit − yjt | e = − |e − e | Sij,t it jt I

where

yit = αi + γ t + eit

Then can estimate β over time, in deviations from country-pair averages αij : Sij,t = αij + γ t + β · Kij,t + δ · Zij,t + η ij,t

I

Kalemli-Ozcan, Papaioannou and Peydro (2013, JF): 18 OECD countries over 1978-2006 β < 0 ⇒ Negative correlated cycles

I

But common shocks pollute this estimation – if they have country-specific loadings

Measures of business cycle synchronization & Common shocks

11

Why common shocks matter

I

Suppose true model is: yi,t = ayi + byi Fty + εyi,t where Ft is a vector of common factors

I

Then Sijt embeds heterogeneous responses to common shocks: � � Sij,t = − ayi − ayj + byi − byj Fty + εyi,t − εyj,t

I

e . True of both Sij,t and Sij,t

Measures of business cycle synchronization & Common shocks

12

Plan

I

Measures of business cycle synchronization & Common shocks

I

Estimation & Data

I

Results

I

Interpretation

I

Conclude

Estimation & Data

13

Data: Sample

I

Data is extension of Kalemli-Ozcan, Papaioannou, Peydro (JF, 2013)

I

KPP data set covers 18 advanced economies • Australia, Austria, Belgium, Canada, Switzerland, Germany, Denmark,

Spain, Finland, France, UK, Ireland, Italy, Japan, Netherlands, Portugal, Sweden, and US • 153 country pairs I

Annual data from 1980 to 2012

Estimation & Data

14

Banking integration measures I

Virtually non existent time varying measures of international capital but for bank assets and liabilities

I

“International Locational Banking Statistics Database” provided by the BIS • Asset (Aij ) and liability (Lij ) of banks located in i (the “reporting

area”) held in country j (the “vis-a-vis area”) I

Two measures: normalized by population or by GDP pop Kij,t =

1 4

h

gdp Kij,t =

1 4

h

Estimation & Data

ln

�

ln

Aij,t Pi +Pj

�

Aij,t Yi +Yj

�

+ ln

�

Lij,t Pi +Pj

�

+ ln

�

Aji,t Pi +Pj

�

+ ln

�

Lji,t Pi +Pj

�i

�

+ ln

�

Lij,t Yi +Yj

�

+ ln

�

Aji,t Yi +Yj

�

+ ln

�

Lji,t Yi +Yj

�i

15

Banking integration measures

-12

-6

-12.5

-6.5

-13

-7

-13.5

-7.5

-14

-8

-14.5

K

pop

(left ax.)

K

gdp

(right ax.)

-15

-8.5

-9 1983

1987

1991

1995

1999

2003

2007 pop

2011 gdp

Note. The solid and dotted lines plot the evolution over time of the average value of Kij,t and Kij,t for the 1980-2012 period. The average is computed across 153 country pairs (our sample spans 18 countries) for each year.

Estimation & Data

16

Synchronization measures we consider I

Consider the following measures � � Sij,t = − ayi − ayj + byi − byj Fty + εyi,t − εyj,t � � F = − by − by F y Sij,t i t j ε = − εy − εy Sij,t i,t j,t

I

F and S ε are the components of S Sij,t ij,t associated with common ij,t and idiosyncratic shocks, respectively

I

Use either measure in conventional panel regression Sij,t = αij + γ t + β · Kij,t + δ · Zij,t + η ij,t OLS between, then OLS within. With or without trade controls.

Estimation & Data

17

How to proxy for unobserved common factors?

I

Objective Compute country-specific decompositions of the type y y yi,t = ayi + by1,i F1,t + ... + byn,i Fn,t + ν yit

I

Simple methodology: extract the first n principal components (Ftn ) from the panel (28 years × 18 countries) of GDP growth rates

I

How many principal components? Retain principal components as long as their associated eigenvalue is > 1

Estimation & Data

18

How to proxy for unobserved common factors? Factor estimates

F1 F2 F3 F4 F5

Eigenvalues

Share of variance

Cum. share of variance

yi t

yi t

yi t

10.67 2.21 1.02 0.89 0.83

59% 12% 6% 5% 5%

59% 72% 77% 82% 87%

I

y y y F using fitted values a Compute Sij,t ˆi + ˆby1,i Fˆ1,t + ˆby2,i Fˆ2,t + ˆby3,i Fˆ3,t

I

ε using residuals ν y Compute Sij,t it

Estimation & Data

19

What do our synchronization measures look like? 0

-0.5

-1

-1.5

-2

-2.5

-3 1983

1987

1991

1995

1999

2003

2007

2011

S

Note. The solid line plots the evolution over time of the average value of Sij,t for the 1980-2012 period. The average is computed across 153 country pairs (our sample spans 18 countries) for each year. The chart also reports the cross-sectional averages of the idiosyncratic component (dashed line) and the common component (dotted line) of Sij,t . Ft has been proxied by the first 3 principal components on the full panel of GDP growth rates. The averages are computed across 153 country pairs for each year over the 1980-2012 period.

Estimation & Data

20

What do our synchronization measures look like? 0

-0.5

-1

-1.5

-2

-2.5

-3 1983

1987

1991

1995 S

1999 S

F

S

2003

2007

2011

ǫ

Note. The solid line plots the evolution over time of the average value of Sij,t for the 1980-2012 period. The average is computed across 153 country pairs (our sample spans 18 countries) for each year. The chart also reports the cross-sectional averages of the idiosyncratic component (dashed line) and the common component (dotted line) of Sij,t . Ft has been proxied by the first 3 principal components on the full panel of GDP growth rates. The averages are computed across 153 country pairs for each year over the 1980-2012 period.

Estimation & Data

21

Plan

I

Measures of business cycle synchronization & Common shocks

I

Estimation & Data

I

Results

I

Interpretation

I

Conclude

Results

22

OLS “between” estimates (1980–2012)

Banking / Pop. (K

pop

)

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

0.095 (0.011) [8.70]

0.106 (0.008) [12.85]

0.038 (0.007) [5.43] 0.091 (0.010) [9.52]

0.082 (0.007) [11.31]

0.049 (0.006) [7.98]

4863 0.095 153

4863 0.170 153

4863 0.127 153

Banking / GDP (K gdp )

Observations R2 Country Pairs

4863 0.092 153

4863 0.176 153

4863 0.121 153

Note. All regression specifications include a vector of year fixed effects. Estimation is performed over the 1980-2012 period.

Results

23

OLS “within” estimates (1980–2012)

Banking / Pop. (K

pop

)

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

-0.144 (0.040) [-3.63]

-0.154 (0.030) [-5.05]

0.075 (0.021) [3.54] -0.148 (0.042) [-3.56]

-0.159 (0.032) [-4.98]

0.072 (0.022) [3.28]

4863 0.099 153

4863 0.222 153

4863 0.133 153

Banking / GDP (K gdp )

Observations R2 Country Pairs

4863 0.099 153

4863 0.222 153

4863 0.133 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2012 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Results

24

OLS “within” estimates with controls (1980–2012)

Banking / Pop. (K

pop

)

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

-0.102 (0.040) [-2.57]

-0.132 (0.028) [-4.71]

0.060 (0.024) [2.55] -0.137 (0.029) [-4.65] -0.203 (0.113) [-1.79]

0.056 (0.024) [2.32] 0.141 (0.078) [1.81]

4859 0.225 153

4859 0.134 153

Banking / GDP (K gdp )

Trade

Observations R2 Country Pairs

-0.382 (0.134) [-2.86]

-0.198 (0.114) [-1.75]

0.132 (0.078) [1.69]

-0.106 (0.041) [-2.55] -0.386 (0.133) [-2.90]

4859 0.103 153

4859 0.224 153

4859 0.134 153

4859 0.103 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2012 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Results

25

OLS “within” estimates (1980–2006)

pop

Banking / Pop. (Φ

)

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

-0.280 (0.063) [-4.46]

-0.314 (0.052) [-6.04]

0.091 (0.028) [3.22] -0.284 (0.066) [-4.33]

-0.321 (0.054) [-5.91]

0.085 (0.029) [2.91]

3945 0.118 153

3945 0.181 153

3945 0.102 153

Banking / GDP (Φgdp )

Observations R2 Country Pairs

3945 0.118 153

3945 0.183 153

3945 0.102 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2006 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Results

26

Endogeneity

I

Endogeneity is an obvious concern for OLS estimates above

I

Kalemli-Ozcan, Papaioannou, Peydro (2013) introduce instruments for bank cross-holdings: Kij,t = δ ij + δ t + γ · HARM ONij,t + ξ ij,t Sij,t = αij + αt + β · BAN KIN Tij,t−1 + η ij,t

I

Results

HARM ON is an index of legislative harmonization policies in financial services for 13 EU countries, from 1999 to 2006

27

IV “within” estimates (1980–2006)

pop

Banking / Pop. (Φ

)

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

-0.487 (0.132) [-3.69]

-0.367 (0.084) [-4.35]

0.237 (0.089) [2.66] -0.519 (0.141) [-3.69]

-0.391 (0.090) [-4.35]

0.253 (0.095) [2.66]

3951 0.110 153

3951 0.185 153

3951 0.046 153

Banking / GDP (Φgdp )

Observations R2 Country Pairs

3951 0.112 153

3951 0.188 153

3951 0.054 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2006 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Results

28

Time variation in factor loadings I

Parameter (ie, factor loadings) stability is another obvious concern for OLS estimates above

I

Consider the following model for GDP growth: yt = ayt + byt Fty + eyt

I

Let Xt = (1, Fty ) and β t = (ayt , byt )0 . Cast in state-space form: yt = Xt β t + eyt β t = β t−1 + vt

I

Results

Estimate via Gibbs sampling

29

OLS “within” estimates with time varying factor loadings (1980–2012)

Banking / Pop.

S

SF

Sε

S

SF

Sε

(1)

(2)

(3)

(4)

(5)

(6)

-0.144 (0.040) [-3.63]

-0.195 (0.037) [-5.21]

0.033 (0.012) [2.68] -0.148 (0.042) [-3.56]

-0.199 (0.040) [-5.03]

0.031 (0.013) [2.46]

4863 0.099 153

4863 0.197 153

4863 0.161 153

Banking / GDP

Observations R2 Country Pairs

4863 0.099 153

4863 0.198 153

4863 0.161 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2012 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Results

30

Plan

I

Measures of business cycle synchronization & Common shocks

I

Estimation & Data

I

Results

I

Interpretation

I

Conclude

Interpretation

31

[Quick reminder on the notation] I

Model for GDP growth: yi,t = ayi + byi Fty + εyi,t

I

Definition of synchronization: � � Sij,t = − ayi − ayj + byi − byj Fty + εyi,t − εyj,t � � F = − by − by F y Sij,t i t j ε = − εy − εy Sij,t i,t j,t

I

Baseline regression: Sij,t = αij + γ t + β F · Kij,t + δ · Zij,t + η ij,t

Interpretation

32

Why the reversal? I

Assume that common shocks (with heterogeneous effects) also affects capital: K K K Kij,t = aK ij + bij Ft + εij,t See: Forbes and Warnock (2012), Rey (2013), Bruno and Shin (2014)

I

F Consider our baseline regression with Sij,t

� � � � K K K F − byi − byj Fty = αij +γ t +β F · aK ij + bij Ft + εij,t +δ·Zij,t +η ij,t I

Sign of β F is given by: � y � K − byi − byj · bK ij Cov |Ft | , Ft

Interpretation

33

Permanent Features?

I

Suppose � �now a systematic positive correlation exists between y y bi − bj and bK ij • E.g., in response to common shocks, capital flows more between

countries with larger differences in GDP elasticity (high byi − byj ) I

F and K Then a negative correlation exists between Sij,t ij,t , and it is driven by permanent features of GDP and capital flows

I

Empirical question: do high bi countries also display high bK ij ?

I

ˆK Plot estimates of ˆb1,i against ˆbK 1,i , where b1,i =

Interpretation

1 J

P ˆK b1,ij j

34

Permanent Features? 0.30 IRL CHE

DNK

DEU USA

0.25

NLD

GBR

AUT

FRA

SWE BEL

ITA

CAN Capital Loading

JPN 0.20 y = 0.04 + 0.78 x [0.4] [1.9]

ESP

0.15

0.10

PRT

FIN

AUS 0.05

0.00 0.10

0.15

0.20 GDP Loading

0.25

0.30

y Note. On the horizontal axis is the loading on GDP (ˆ b1,i ). On the vertical axis is the loading on capital ˆ bK 1,i , where P ˆK K 1 ˆ b1,i = J b1,ij is the average capital loading in country i. The slope and the constant of the fitted line are reported j

together with t-Statistics in square brackets.

Interpretation

35

Permanent Features?

I

ˆK ˆ ij,t = a Also implies that capital (K ˆK ij + bij Ft ) should go to countries with elastic GDP in periods of global (or regional) booms (Ft > 0), but from them in years of global recession (Ft < 0)

I

Define the average change in net bank holdings, computed for positive or negative values of Ft : KN ETi+

=

X

∆t

" X

Ft >0

ln (Aji,t + Lij,t ) − ln (Aij,t + Lji,t ) ,

j

and:

#

" KN ETi−

=

X Ft <0

Interpretation

#

∆t

X

ln (Aji,t + Lij,t ) − ln (Aij,t + Lji,t )

j

36

Permanent Features?

(a) Ft > 0

(b) Ft < 0 0.05

CHE

0.04

ESP

0.02

NLD

DNK

FRA

USA 0.00

GBR

CAN

-0.02

y = -0.08 + 0.33 x [-2.3] [2.0]

ITA

FIN AUT

IRL

BEL

DEU

-0.04

SWE

-0.06

AUS JPN

-0.08 0.10

0.15

PRT

0.20 GDP Loading

PRT

0.04

Average change in net bank holding

Average change in net bank holding

0.06

y = 0.03 - 0.18 x [1.4] [-1.7]

0.03 0.02

JPN

0.01 0.00 -0.01

CHE GBR CAN DEU NLD AUT IRL FIN USA

AUS

-0.02

0.30

FRA

-0.03 SWE

-0.04 0.25

ESP

DNK

ITA

-0.05 0.10

BEL 0.15

0.20 GDP Loading

0.25

0.30

y Note. On the horizontal axis is the loading on GDP (ˆ b1,i ). On the vertical axis is the change in net bank holdings averaged + over periods when Ft > 0 (KN ETi ), in panel (a); and when Ft < 0 (KN ETi− ), in panel (b). The slope and the constant of the fitted line are reported together with t-Statistics in square brackets.

Interpretation

37

This paper

I

Commonly used measures of synchronization are polluted by the impact of common shocks with heterogeneous loadings

I

Heterogenous loadings can explain the negative relation between financial linkages and synchronization

I

Conditional on idiosyncratic shocks financial linkages do not decrease synchronization, sometimes increase it

I

Since theory builds from idiosyncratic shocks, evidence suggests that credit market imperfections may be relevant empirically

Interpretation

38

Appendix

Appendix

39

Time-varying factor loadings United States 0.25 0.2

United Kingdom

Austria

0.3

0.3

0.2

0.2

0.1

0.1

0.15 0.1 1986 1992 1998 2004 2010

1986 1992 1998 2004 2010

Belgium

1986 1992 1998 2004 2010

Denmark

France

0.4

0.4

0.3

0.2

0.3

0.2

0

0.4

0.2

1986 1992 1998 2004 2010

0.1 1986 1992 1998 2004 2010

0.3

0.2

0.2

0.1

0.1 1986 1992 1998 2004 2010

Netherlands 0.3

0.3 0.2

1986 1992 1998 2004 2010

Italy

Germany

0.1 1986 1992 1998 2004 2010

1986 1992 1998 2004 2010

Note. Mean (dotted line) and median (solid line) estimates of the time-varying parameters model. Shaded areas display the 68 percent credible intervals. The dashed line reports the OLS fixed estimates.

Appendix

40

Time-varying factor loadings (2) Sweden

Switzerland

Canada

0.4

0.4

0.3 0.3

0.3 0.2

0.2

0.1

0.1 1986 1992 1998 2004 2010

0.2 0.1 1986 1992 1998 2004 2010

Japan

1986 1992 1998 2004 2010

Finland

0.4

0.4

0.2

0.2

Ireland 0.3 0.2 0.1

0

0 1986 1992 1998 2004 2010

1986 1992 1998 2004 2010

0.4

1986 1992 1998 2004 2010

Spain

Portugal

Australia

0.3

0.2

0.3 0.1

0.2

0.2

0

0.1

0.1 1986 1992 1998 2004 2010

1986 1992 1998 2004 2010 Time-varying

Appendix

16/84 Percentile

1986 1992 1998 2004 2010

Fixed (OLS)

41

OLS “within” estimates (1980–2012) – Pearson correlation

Banking / Pop. (K

pop

)

ρ

ρF

ρε

ρ

ρF

ρε

(1)

(2)

(3)

(4)

(5)

(6)

-0.102 (0.061) [-1.67]

-0.031 (0.015) [-2.07]

-0.017 (0.020) [-0.83] -0.110 (0.064) [-1.74]

-0.033 (0.016) [-2.11]

-0.018 (0.021) [-0.85]

915 0.123 153

915 0.260 153

915 0.001 153

Banking / GDP (K gdp )

Observations R2 Country Pairs

915 0.122 153

915 0.259 153

915 0.001 153

Note. All regression specifications include a vector of country-pair fixed effects and a vector of year fixed effects. Estimation is performed over the 1980-2012 period. Standard errors are adjusted for country-pair-level heteroskedasticity and autocorrelation.

Appendix

42

Factor estimates for capital

F1 F2 F3 F4 F5

Appendix

Eigenvalues

Share of variance

Cum. share of variance

Kij,t

Kij,t

Kij,t

13.15 2.89 0.79 0.66 0.27

73% 16% 4% 4% 2%

73% 89% 93% 97% 99%

43