12 August 2014

Chip Eng Seng

Alexandra Central TOP in Q4 2014

Trading Buy

SINGAPORE | CONSTRUCTION | TRADING BUY Rating: f

Investment Merits More than 30 years of successful track record in public and private housing. It can keep construction cost lower than other developers, by virtue of the fact that it is a main contractor itself. Translates into lower breakeven cost. $548m construction order book, which could be replenished given that BCA expects overall strong construction demand of $31-38 billion this year. Alexandra Central strata retail mall is 98% sold. Lump sum profit recognition upon Q4 2014 TOP, amounting to estimated $152m (30% market cap). Park Hotel Alexandra adds another $139m revaluation surplus when completed. Belvia, Junction Nine substantially sold. Fulcrum@Fort Road is only 18% sold, but unlikely to require write-down as its breakeven is substantially below ASP. Management owns 30% CES, and appears to be savvy at capital deployment. Repurchased 25.1m shares since the start of 2012, at average cost of $0.64. 4-cent annual dividend appears to be sustainable for next 3 years, based on development pipeline and recurring income from its investment properties. Perceived Risks Fewer construction jobs going forward, likely depressing segment margins. Development pipeline in Singapore appears to be drying up beyond 2016. CES recently won a state tender for two plots of land in Fernvale that can be developed into combined 1.1m sqft GFA residential, although that is likely for purpose of keeping its construction arm occupied rather than profit-driven. CES share price might not react dramatically to Alexandra Central TOP in Q4 2014, if expectations of lump sum profit are already baked into its share price. Currency and regulatory risks associated with Australia, Malaysia.

2012 617 81 71.0 12.3 4.0 5.3

2013 503 73 77.1 11.3 4.0 5.4

1,080

3M Average Daily T/O ('000)

1,270.3

Closing Px in 52 wk range

0.64

0.85

1 0.9 0.8 0.7 0.6 0.5 0.4

10.0 8.0 6.0

4.0 2.0 0.0

Vol, mn

Major Shareholders 1. Lim Tiam Seng 2. Lim Tiang Chuan 3. Kenyon Pte Ltd

CHIP SP Equity

Aug-14

2011 360 124 63.0 18.7 4.0 8.1

529

Ent. Value (SGD mn)

May-14

2010 477 175 48.6 26.5 4.0 8.9

0.94

Market Cap. (SGD mn)

Feb-14

Total Revenue $'m Profit After Tax $'m NAV Per Share (cent) EPS Per Share (cent) Dividend Payout (cent) Dividend Yield % Source: SGX Filings, PSR est.

2009 376 51 25.0 7.7 3.0 7.9

Company Data Raw Beta (Past 2yrs weekly data)

Nov-13

Key Financial Summary (SGD)

1.03 0.04 0.83 28.9%

Company Description Chip Eng Seng Corporation Ltd (“CES”) is one of Singapore’s leading main contractors and property developers and has been listed on the Mainboard of SGX since 1999. CES is principally engaged in the key business segments which comprise Construction, Property Developments and Investments as well as Hospitality.

Aug-13

Investment Actions We initiate a TRADING BUY recommendation on Chip Eng Seng at $0.83 with 12month target price of $1.03, representing 29% upside inclusive of 4-cent dividend. This reflects 637m issued and outstanding shares (excluding treasury shares), and doesn’t reflect further share buybacks that would likely be value accretive.

Target Price (SGD) Forecast Dividend (SGD) Closing Price (SGD) Potential Upside

STI rebased

(%) 9.4 6.9 4.5

Valuation Method SOTP Valuation Analyst Wong Yong Kai

[email protected] +65 6531 1685

Page | 1 MCI (P) 046/11/2013 Ref. No.: SG2014_0129

Chip Eng Seng 12 August 2014 Company Background Chip Eng Seng (“CES”) is one of Singapore’s leading main contractors and property developers, and listed on the SGX Mainboard since 1999. It started as a subcontractor firm for conventional landed properties in the 1960s, and has since built up a good reputation for quality and reliability. In 1982, CES won its first HDB project as a main contractor, which eventually paved the way to it being awarded the contract for the iconic Pinnacle @ Duxton, which has since been completed. Today, CES is principally engaged in the following business segments: CONSTRUCTION CES has an A1 grading as a general building and civil engineering contractor registered with the BCA, which permits it to tender for public sector projects of unlimited value. Its core competencies lie in private and public housing (HDB) given its 30+ years of track record, and has $548m external order book as of 30 June 2014. Meanwhile, CES is also working on wholly owned projects, ie. Fulcrum@Fort Road and Junction Nine & Nine Residences, which are negotiated internally at arms length and by our estimates, amount to roughly $100m contract value. Hence, the total order book (external + internal) adds up to $648m. Given that most SGX-listed construction firms also have sizeable property development arms, we have narrowed down to 4 competitors that are either pure-plays (Soilbuild, Logistics), or a smaller exposure to property development (Keong Hong, BBR). Applying blended valuation of 18% order book, this segment is valued at $116m. On the other hand, net assets attributable to this segment are $58m as of 31 Dec 2013, and we adopted the assumption that this figure remains unchanged. Net increase to RNAV (if this segment were carried at fair market value), is $58m. Note that this valuation doesn’t factor in further contract wins, although a shrinking order book can conversely reduce our valuations. In addition, the size of the order book doesn’t reveal any clues about profitability and margins. For instance, CES earned 5.9% pre-tax margins from its construction contracts in 2013, even as BBR Holdings earned only 1.9% pre-tax margins in the same year. Also, CES management revealed they have been awarded tenders although they are not the lowest bidder, because HDB recognizes and values the reliability CES has delivered. That being said, the construction industry faces certain headwinds as private sector projects dry up amidst a soft residential market, and HDB is expected to reduce the supply of BTOs going forward after ramping up in the past 3 years. Fewer jobs would lead to greater competition and depresses margins. Many players are privately-owned, competing not just on price but quality as well. CONQUAS is a benchmark used to assess and score worksmanship quality – China Construction & Qingjian have repeatedly scored among highest for HDB projects. CES would need to supplement external tender awards with internal development projects to fill up its order book pipeline and keep its construction arm occupied.

Page | 2

Chip Eng Seng 12 August 2014 PROPERTY DEVELOPMENT & INVESTMENT CES had historically completed more than 10 property developments locally and overseas in Australia. Currently, it has the following projects in the pipeline: 1. Alexandra Central (Hotel + Strata Retail)

In December 2011, CES was the highest among six bidders for this 99-year leasehold site at Alexandra Road, paying $789 psf ppr for the land. Fortunately, this bid was just 2.7% higher than the second bidder. This project was renamed Alexandra Central, divided into a 450-room four star hotel to be managed by Park Hotel Group, and 93,080 sqft GFA strata retail mall. In January 2013, it proceeded to launch strata retail units – buyers quickly snapped up the units at average selling price (ASP) of $5,044 psf (Source: URA Realis), and today it is 98% sold. CES announced that this project will cost $350m, and had allocated $66.4m of the $189m land cost to the strata retail component. If we apply a similar allocation ratio for construction cost ($101m construction contract were tendered to Keong Hong), and factoring in miscellaneous professional fees, financing and marketing expenses, the breakeven cost for strata retail area works out to $118m. At 65% efficiency, after-tax profits recognizable upon Q4 2014 TOP is $152m. Meanwhile, Alexandra is untested for hotels, hence there are no comparable data for room rates or occupancies. Notably, CES was previously offered $820,000 per key to sell the entire hotel, which the Board turned down as there is no better alternative to recycle this capital. Besides, expanding into hospitality sector would provide CES with recurring income. If the 450-room hotel were valued using the same metric, it would be worth $369m => Revaluation Surplus = $139m. Every $100,000 per key increment to the hotel’s value increases RNAV by 7 cents. However, there is no current intention to put up the hotel for sale, hence shareholders would benefit mostly from recurring income and rising asset value.

Page | 3

Chip Eng Seng 12 August 2014 2. Junction Nine & Nine Residences

In January 2013, CES submitted the top bid of $212.1m for this 99-year leasehold site at Yishun Ave 9, translating into $794 psf ppr, and outbidding 12 other developers including the JV between Far East Organization and Far East Orchard, who came in second with $726 psf ppr bid. This site was launched in Oct 2013, comprising of 106,788 sqft GFA strata retail mall (Junction Nine) that is 98% sold, and 186-unit 176,200 sqft GFA condominium (Nine Residences) that is 77% sold. By our calculations, the residential component should have a breakeven cost of $869 psf, significantly below the $1,063 psf ASP. As such, we are comfortable with the somewhat slow sales, and indeed encouraged that 25 units were moved in the past half year amidst the soft residential market. Remaining unsold 42 units could be gradually taken up over the next 1 year; in any case, expected TOP is 2016. In the meantime, Junction Nine commanded $3,490 ASP. Given that revenue from this development is recognized progressively (percentage-of-completion method), we calculate the yet-to-be-recognized profits from already sold units to be $39m. It is worth noting that in Frasers Centrepoint clinched a nearby plot of land for $1,077 psf ppr, although they are not directly comparable for two reasons: I) Frasers’ site is strategically located directly beside the Yishun MRT station, whereas Junction Nine is slightly further – 1km and two traffic lights away. II) Frasers already owns the shopping mall Northpoint, and is strongly keen to maintain its presence. Indeed, their top bid is 47.4% above the second bid. Nonetheless, the high land cost ought to indirectly provide a price support for the remaining unsold Nine Residences. In fact, the upcoming launch of nearly 1,000 condominiums at this Frasers’ site might reignite interest at Nine Residences.

Page | 4

Chip Eng Seng 12 August 2014 3. Fulcrum@Fort Road

In March 2010, CES was granted an option to buy 16 freehold terrace houses in Tanjung Rhu for $86 million. It subsequently launched the 100,544 sqft GFA, 128unit freehold condominium as Fulcrum@Fort Road in April 2012 at $1,960 ASP, and has sold 17 units to date. Project expected to TOP in 2016, after which QC conditions kick in and require the balance units to be sold two years later by 2018. At $1,657 psf breakeven cost, it’s unlikely to need write-down. Even if a writedown is necessary, the quantum shouldn’t be significant. Nearby, The Line @ Tanjong Rhu (uncompleted) sold 41 units at $2,246 psf ASP, while freehold The Waterside (completed in 1992) fetched $1,373 psf ASP in the resale market even though all units are larger than 2,000 sqft, vs Fulcrum’s average 723 sqft unit size. For perspective, $100 psf write-down of the unsold units (in other words, 20% price reduction from its current $1,960 ASP) translates into $7.6m pre-tax losses, a pittance compared to its $510m market cap, and unlikely to register much of a blip.

Page | 5

Chip Eng Seng 12 August 2014 4. Belvia DBSS

In December 2010, CES won a tender for its first DBSS project at Bedok Reservoir Crescent, bidding $112.7m for the site translating into $224 psf ppr. It is more than 99% sold – 486 out of the 488 units taken up, and expected to TOP in Q3 2014. At $495 psf breakeven cost and $571 psf ASP, we estimate profits to be $30m.

5. CES Centre (formerly San Centre)

In March 2013, CES purchased San Centre, a 12-storey office building with 131,895 sqft GFA, for $113m, which works out to $857 psf GFA. The property is of 99-year leasehold tenure from 02 June 1969, hence it has 54 years lease remaining. San Centre has since been renamed CES Centre, and is fully vacated while undergoing addition and alteration works. Upon completion, 2 floors would be used as CES office, and the remaining 10 floors would be leased out to generate rental income. CES Centre has some redevelopment potential, given the prime location (10mins walk from Chinatown MRT), possible alternative uses, and less than 60 years lease. Indeed, word on the street is that the site could be redeveloped into 20-storey hotel, or mixed development with at least 60% space set aside for commercial use. Redevelopment is unlikely in the near term though, as CES is spending $20m on addition & alteration works. Instead, CES Centre could be viewed as landbank that is likely to be worth more in the future. We have not assigned any revaluation surplus, until there is more visibility on the occupancies and psf rental rates.

Page | 6

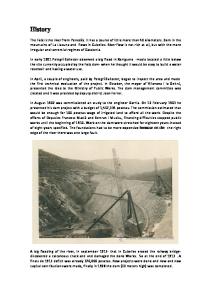

Chip Eng Seng 12 August 2014 6. Australian Real Estate

In December 2013, CES purchased 11-storey freehold office building (above picture) at 420 St Kilda Road, Melbourne, for A$45.3m. The 10,528 sqm NLA property is fully tenanted and initially generates 8.1% rental yield. CES is currently occupying 1 storey, and intends to hold the property for investment purposes. Other tenants include ANZ Business Centre, Intergraph Corporation, and Harris Scarfe. It also has a freehold Tower Melbourne residential development that sits on a site area of 913 sqm, and is substantially sold (578 of 581 units). However, it is facing delays in securing approval for demolition works. As such, TOP (and by extension, profit recognition) is expected only in 2018. Given that CES had previously completed 2 developments (North Shore and 33M) in Australia, we are comforted that it has the relevant experience to secure the necessary permits and approvals. Irregardless, even in the worse-case scenario whereby CES has no choice but to abandon Tower Melbourne project, they can simply refund buyers, partition the superstructure, then refurbish for leasing, and still pocket 8-9% yield on cost. Lastly, CES also wholly owns 3 other freehold land banks measuring 41,094 sqm in Perth and Melbourne, with a total acquisition cost of A$71.3m. 2 of the 3 sites would be launched in Q4 2014 and 2015, with plans to build more than 1,000 residences. Again, we have not factored in any development profits or revaluation surplus, given concerns over Australia’s high housing prices and slower GDP growth, and that profit recognition for the developments are in 2018 and after.

7. In-The-Works Pipeline Malacca: In April 2014, CES announced that it is in the midst of acquiring a site, with a total land area of 4,120 sqm, for RM19m. If the purchase goes through, the development would comprise primarily of hotel and serviced apartments. Fernvale: In August 2014, CES announced that its 60%-owned SPV emerged as the top bidder for two plots of land, with a combined maximum 1.1m sqft GFA, for a price of $487m, ie. $443 psf ppr. The development is located near the upcoming Seletar Mall and yields 1,400 condominiums. While we are excluding its share of development profits pending more clarity on plans and launch prices, we note the nearby Fernvale@Riverbank sold for $1,023 ASP. Assuming small discount for nonwaterfront living, we estimate that it should at least break even, while adding to its construction pipeline. On the other hand, $50 psf profit boosts RNAV by 4 cents.

Page | 7

Chip Eng Seng 12 August 2014 Capital Management We understand from CES management that they are inclined to retain profits recognized from sale of Alexandra Central strata retail units, and we speculate that this capital would be likely recycled into Fernvale project given its 60% share of land cost is $292m. Hence special dividends, if declared, shouldn’t be substantial. Another question that most investors would ask, is whether the 4-cent dividend since 2010 sustainable? This payout equals $25.5m cash outflows every year. 1. Average of $90m development profits from now till 2016. 2. Park Hotel Alexandra ($190 RevPar), 420 St Kilda Rd and CES Centre = $2.1m + $3.7m + $10.4m = $16.2m after-tax income when stabilized. Its 3 investment properties should yield approximately $16.2m, or 2.5-cent EPS. Combined with the average of $90m development profits to be recognized from now till 2016, it seems that the 4-cent dividend ought to be safely covered and sustainable for the next three years, beyond which there is not enough visibility.

Valuation & Target Price Chip Eng Seng NAV (30 June 2014) $512m 1. Construction Arm + $58m 2. Development Profits a) Alexandra Central - Strata Retail Mall b) Junction Nine Project c) Fulcrum @ Fort Rd d) Belvia DBSS Subtotal

+ $152m + $39m + $4m + $30m__ + $225m

3. Revaluation Surplus a) Alexandra Central - 450-room Hotel RNAV (30 June 2014)

+ $139m_ $934m

$934m RNAV works out to $1.47/share. Applying 30% discount to its RNAV, we arrive at a target price of $1.03, which is 24% higher than today’s share price.

Overall Conclusion CES has had a good track record as a main contractor, and completed more than 10 residential developments to date. Management owns 30% of the company, and appears to be shareholder friendly having declared 4-cent dividend annually since 2010 (works out to 5-9% gross dividend yield based on the closing share price), and which we have earlier estimated to be sustainable for the next three years. Meanwhile, we have conservatively valued its RNAV to be $1.47/share, a figure that has yet to factor in development profits from Australia, Malacca and Fernvale, nor revaluation surplus from its two investment properties CES Centre and 420 St Kilda Rd. Given CES successful track record, prudent approach to development projects, and shrewd timing of the property market, 30% discount to RNAV ought to be sufficient, and shareholders could be richly rewarded if the market awakens to its $152m windfall when Alexandra Central’s strata retail mall TOP in Q4 2014.

Page | 8

Chip Eng Seng 12 August 2014 For Financial Summary at the end of report

FYE Dec Income Statement (SGD mn) Revenue Cost of Sales Other Items of Income Int & Div Income Other Income Other Items of Expense Marketing & Distribution Administrative Expenses Finance Costs Share of Results of Associates Profit Before Tax Income Tax Expense Net Income FYE Dec Cashflow Statements (SGD mn) Profit Before Tax Depreciation & Amortization Share of Results of Associates Net FV Gain on Inv Properties Other Items Combined OCF Before Changes in WC Development Properties Trade & Other Receivables Trade & Other Payabes Other Items Combined Income Taxes Paid Cashflow from Operations PPE & Investment Properties Other Items Combined Cashflow from Investing Loans & Borrowings Dividends Paid Share Buybacks Cashflow from Financing Increase in Cash & Equivalents Cash & Equivalents (Beginning) Cash & Equivalents (Ending) Source: Company Data, PSR est

2010

2011

2012

2013

477 (418)

360 (220)

617 (487)

503 (413)

4.8 3.1

2.0 8.3

3.8 32.4

2.3 14.9

(14.0) (12.7) (17.5) (18.9) (1.5) (0.2) 144 23.8 177.1 141.9 (2.8) (18.3) 174 124

(30.7) (27.8) (1.0) 2.2 109 (27.3) 81.3

(20.5) (28.4) (2.0) 29.9 85.4 (12.0) 73.4

2010

2011

2012

2013

177 1.5 (144) (1.5) (17.1) 16.4 (200) 27.1 (21.4) 17.2 3.0 (158) (5.7) 134.4 129 171 (20) (65) 86.5 57.5 76.1 133.6

142 1.1 (23.8) (5.5) 1.8 116 (115) (34) (29.1) (99.8) (0.8) (162.6) (6.5) 130.6 124 124.7 (26.5) (37.5) 60.7 22.2 133.6 155.8

109 3.1 (2.2) (30.0) (3.1) 76.4 35 15.5 (33.2) 78.2 (35.0) 137 (136) 67.8 (68.4) 52.2 (27) (7.7) 18.0 86.3 155.8 242.1

85.3 3.5 (29.9) (13.0) (11.1) 34.8 (107) 22.7 (6.9) (51.0) (5.8) (114) (136) 12.4 (124) 306.8 (25.9) (1.1) 280 42.2 242.1 284.3

FYE Dec Balance Sheet (SGD mn) Property, Plant & Equipment Investment Properties Investment in Associates Other Assets Non-Current Assets Gross Amt due from customers for contract work-in-progress Completed Properties (HFS) Development Properties Prepayments & Deposits Trade & Other Receivables Cash & Short-Term Deposits Current Assets Total Assets Loans & Borrowings Gross Amt due to customers for contract work-in-progress Trade & Other Payables Other Liabilities Current Liabilities Loans & Borrowings Deferred Tax Liabilities Non-Current Liabilities Total Liabilities Non-Controlling Interests Shareholder Equity Growth & Margins (%) Growth Revenue Net Income Shareholder Equity Margins Gross Profit Margin Net Profit Margin Key Ratios ROE (%) ROA (%)

2010 7.0 96.5 110 46.0 260 0.6

2011 11.7 139.4 12.8 53.3 217 2.7

2012

2013

145 44.7 5.0 12.0 207 7.5

162 176 28.4 13.5 380 11.2

2.8 319 43.2 84.3 134 583 843 116 106

1.5 458 18.8 136 156 773 990 63 5.7

1.8 544 1.5 152 242 949 1156 123 24.3

0.3 651 8.8 129 284 1,085 1465 281 28.2

99.3 26.6 347.5 169 5.8 175 523 0 320

95.6 54.1 217.9 347 8.7 356 574 0 417

109 96.6 352.7 339 3.7 343 695 0 460

108 47.3 464.1 488 14.5 502 966 0 499

26.7% -24.5% 71.4% -18.6% 131.5% -29.0% -34.3% -9.7% 94.1% 30.2% 10.4% 8.3% 12.3% 36.5%

38.8% 34.4%

21.0% 13.2%

17.8% 14.6%

71.8% 29.2%

33.6% 13.5%

18.5% 7.6%

15.3% 5.6%

*Forward multiples & yields based on current market price; historical multiples & yields based on historical market price.

Page | 9

Chip Eng Seng 12 August 2014 Ratings History

1.20 1.10 1.00 0.90 0.80 0.70 0.60 0.50 0.40

Source: Bloomberg, PSR

Market Price Target Price

Dec-14

Sep-14

Jun-14

Mar-14

Dec-13

Sep-13

Jun-13

Mar-13

Dec-12

Sep-12

Jun-12

1

0 PSR Rating System Total Returns

Recommendation

Rating

> +10% < -10%

Trading Buy Trading Sell

1 0

Remarks We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors like (but not limited to) a stock's risk reward profile, market sentiment, recent rate of share price appreciation, presence or absence of stock price catalysts, and speculative undertones surrounding the stock, before making our final recommendation

Page | 10

12 August 2014 Important Information This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication. The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication. Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results. This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication. Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment. To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material. The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication.

Page | 11

12 August 2014 This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products. Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore. Contact Information (Singapore Research Team) Management Chan Wai Chee (CEO, Research - Special Opportunities) Joshua Tan (Head, Research - Equities & Macro) Equities | Macro Joshua Tan Soh Lin Sin Bakhteyar Osama Finance Benjamin Ong

Telecoms Colin Tan

+65 6531 1249 +65 6531 1516 +65 6531 1793 +65 6531 1535

+65 6531 1221 SINGAPORE Phillip Securities Pte Ltd Raffles City Tower 250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631 Website: www.poems.com.sg

Research Operations Officer Jaelyn Chin +65 6531 1240

+65 6531 1231 +65 6531 1249 Market Analyst | Equities Kenneth Koh +65 6531 1791

US Equities Wong Yong Kai

+65 6531 1685

Real Estate Caroline Tay

Real Estate Lucas Tan

+65 6531 1229

+65 6531 1792

Transport Richard Leow, CFTe +65 6531 1735 Contact Information (Regional Member Companies) MALAYSIA Phillip Capital Management Sdn Bhd B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099 Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd 11/F United Centre 95 Queensway Hong Kong Tel +852 2277 6600 Fax +852 2868 5307 Websites: www.phillip.com.hk

JAPAN Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku, Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090 Website: www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia Tel +62-21 5790 0800 Fax +62-21 5790 0809 Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd No 550 Yan An East Road, Ocean Tower Unit 2318, Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940 Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd 15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak, Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999 Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited 3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France Tel +33-1 45633100 Fax +33-1 45636017 Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited 6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS Tel +44-20 7426 5950 Fax +44-20 7626 1757 Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc 141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

AUSTRALIA PhillipCapital Level 12, 15 William Street, Melbourne, Victoria 3000, Australia Tel +61-03 9629 8288 Fax +61-03 9629 8882 Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited 2nd Floor,Lakshmans Building, No.321, Galle Road, Colombo 03, Sri Lanka Tel: (94) 11 2429 100 Fax: (94) 2429 199 Website: www.ashaphillip.net

INDIA PhillipCapital (India) Private Limited No. 1, C‐Block, 2nd Floor, Modern Center , Jacob Circle, K. K. Marg, Mahalaxmi Mumbai 400011 Tel: (9122) 2300 2999 Fax: (9122) 6667 9955 Website: www.phillipcapital.in

Page | 12